Inmode: destroy the long thesis, 7 risks to consider, selling rules, and Q3 update

Inmode: destroy the long thesis, 7 risks to consider, selling rules, and Q3 update

In my deep dive into Inmode, I postulated a long thesis and listed some risks. The goal is to hold on as long as the thesis is not broken.

But as Charlie Munger says, you should try to destroy a cherished idea once every year. It feels to me that this is what we need to do with any idea. To invert. What are the reasons it could go wrong?

The result of this analysis will be added to my selling rules and the way I will track Inmode in the coming years.

Let’s start with an update on the results of the earnings call yesterday November 2nd, 2023.

What did we learn from the last earnings call?

Conflict in Isräel

All employees are safe. Their production facilities are located in the north and are not in any kind of trouble. Even if for some reason, production would be halted, they have about 2 quarters of inventory to go to finished goods. That is their buffer at this time.

Revenue

Revenue in Q3 was 123M USD, 2% higher than last year. They have confirmed guidance for the entire year. Revenue should arrive at 500 to 510M USD. They need to hit 140M in revenue in Q4 which they think should be possible. 15% of revenue came from consumables which is a bit lower than I expected. We’ll have to wait for the final end-of-year results.

This is the first significant slowdown in the past couple of years, management sees 3 reasons for this slowdown:

Seasonality of the procedures: Management states that before COVID, they observed a seasonality throughout the quarters with Q3 being the worst performer because generally it is summer, and people will do their aesthetic procedures before or after the summer. They claim that due to COVID, this was somewhat displaced, and the past Q3 quarters should be considered an anomaly. We have returned to normal seasonality. I understand the reasoning, but they always talked about seasonality in the past quarters. To claim that all of a sudden past quarters were abnormal seems a stretch to me. I think the following 2 points are more important when regarding the worse performance of this quarter compared to last year. In the CEO’s words:

First, I believe the seasonality, which is now normal in the medical aesthetic, as you probably know, in 2021 and ‘22 was COVID year and COVID was at the beginning of the year and therefore Q3 was much stronger than expected, and sometimes stronger than Q2. But that's not normal in the medical aesthetic. I've been in the medical aesthetic for 25 years all the way for me at C-Luminous, Syneron, and now InMode. And it's always the case that the third quarter summertime, because people don't want to get treatment during the summer and are exposed to the sun on their vacation, it's a slower quarter and the fourth quarter usually is the strongest one.

High-interest rates for the lease agreements: Interest rates for a typical lease agreement for an Inmode platform sit at about 14 to 15%. A typical lease duration is 5 years. These rates have risen sharply in the past year. With these higher interest rates, physicians think twice before buying. The ROI on Inmode’s offering is longer.

So this is one of the reasons and I mean we cannot avoid it. Second, as far as financing, what we said is that today a leasing cost is 14% to 15% annually. That's the interest rate of the leasing company charging customers. So I'm sure that you will not take a mortgage with 14% to 15% interest rate. Although this is a working machine that generates money, the return on investment with this kind of interest rate will take longer. And of course, doctors are afraid what will happen. The economy is slowing down.

Longer screening times for lease contracts. The lending or leasing companies also do a lot more due diligence and take a conservative approach when providing lease agreements. It takes about 2 to 3 weeks now which is too long. Again, a physician might reconsider his investment or a competitor might walk in within this period.

The third reason is the fact that leasing company are tightening their procedure and their screening. They are afraid doctors will go bankrupt and they will not see the money. And therefore before the issue of a purchase order to us to actually take the order, they do a very long, I would say, a very long processing time. Sometimes it takes two to three weeks. And when you have two to three weeks, some of our competitors are coming. Doctors think twice. They already think maybe I need to wait a little bit.

Management has stated that they cannot tackle points 1 and 2, but they will take action to reduce the screening times. Their sizable cash war chest will now prove useful as it allows them to bring more certainty to the leasing agencies. They are negotiating actively with them. A second option is to provide their own financing. They haven’t given any details on this but they are looking into it.

Although Q4 will be their strongest quarter, they do see the start of a slowdown, especially in the US. Growth remains stronger in Asia. The reason why there was such a big difference in the guidance estimate is that 50% of revenue is always generated in the last month of each quarter.

Although they never give details on sales per platform, they did share that their new ocular treatment platform (Envision) has launched well in the US and they are seeing considerable growth.

They emphasize that they will continue to invest in growth, by increasing R&D, hiring additional staff, and making sure that production stays at a high performance. They do not want to start cutting costs.

One last interesting remark on the impact of Ozempic and other GLP-1-related drugs. Management has mentioned in the past that this could be a tailwind for Inmode, because when you lose weight too quickly, your skin is loose, and Inmode can come in to help you. An analyst asked if they had seen patients on Ozempic coming in for treatment. Here’s the reply from the chief medical officer:

I think the one thing I did not mention is the price of these medications, right? I think a person who’s spending $1,500 a month, $2,000 a month to lose weight has already crossed the line to say, you know what, I want to look better and healthier. And the healthier part is secondary. It's usually I want to look better, just the way human nature is. So, you're looking at a patient spending $10,000 to $15,000 in a year on these medications and committed and now they definitely have lost the weight, but they've also looked worse. So, once they've crossed that line, what we're seeing is for them to come in and have things done to spend more money on a Morpheus treatment, for example, which is simple, $3,500 to $4,000. It's not a big deal. So I don't want to say it's sort of like a gateway drug to us, but it kind of is. So I do think it's going to have a positive impact on us.

So, definitely, I think there's going to be a positive impact for us. And the trends so far are looking that way.

Conclusion: Although we can question their capital allocation strategy in the past, the strong cash balance sitting now at 675M USD could be useful to alleviate this financing problem which may gain them a slight edge over competitors. Next year will be difficult with I think an additional slowdown in sales.

Inmode should be careful though, as they mention they may take some of the credit risk from the physicians using their strong balance sheet. This could be an advantage but it also brings in additional risk.

Earnings

The gross margin was stable at about 84%. Although management has stated that prices of components have kept rising in the last 2 years, they have never raised the price on their platforms. They might however raise the price in the future. The fact that they were able to maintain their gross margin is due to production efficiencies in the last few years. This comes back to what I had written in the deep dive on their operational excellence being a competitive advantage.

Earnings per share should arrive at 2.5 USD/share (non-GAAP) for the full year which would lead to a 15% increase compared to last year.

Capital Allocation

I was relieved that one of the analysts asked the question concerning buybacks directly to management. I was however less pleased with their answer:

They are not planning to buy back shares. In fact, the current CEO emphasizes that he might never do it. The 100M USD they have spent in the past (2021 and 2022) did not have the desired effect on the stock price. An example to reinforce their standpoint is Hydrafacial, the flagship product of Beauty Health Co (TICKER: SKIN). They announced a 100M USD share buyback 6 weeks ago and the stock still dropped 30%.

Here are his exact words:

Well, we thought about buyback. We thought about buyback for a long time. But I have to say two things. One, our previous experience with buyback, actually we did buyback for $100 million, did not help, did not help at all. And the stock did not react to that. It was not now, but it did. Second, I'm sure you know that one of our competitors, a company called HydraFacial, which market the product to the same market that we do, mainly to spa and less to doctors, but they sell also to doctors. They have announced six weeks ago that they are doing buyback of $100 million, official buyback, $100 million. We all expected their stock to go up. The stock price when they announced it was $6.3. The stock price today is $4. So they lost 35% of their value in the last six weeks right after they announced the buyback. So it's made us to think twice if this is the best way to support the stock, to do a buyback.

I believe they are looking at this the wrong way. I agree that in theory, in capital allocation, the typical order is the following:

Reinvest in growth

Do M&A

Buyback shares or pay out dividends

But the goal is not to sustain the price in the short-term, the goal is to compare the possible allocation decisions and decide which has the biggest return on invested capital.

Their capital allocation strategy remains acquisitions. There were some prospects during the year, but the price was too high or the acquisition would not have been accretive to the gross margin of Inmode.

They plan to continue investing in R&D and look for acquisition opportunities. The drawdown in the value of their competitors might make it more interesting from a pricing point of view.

We’ll need to track this closely because up until now, there has been a lot of talk. It is time to walk that talk. I hope their patience, and our patience will be rewarded in the future.

Maybe it is us that are wrong. Everybody is asking for buybacks. Maybe they will come up with a great acquisition in the future, at an excellent price because of the drawdown in the market. We’ll have to wait and see.

What is the market saying?

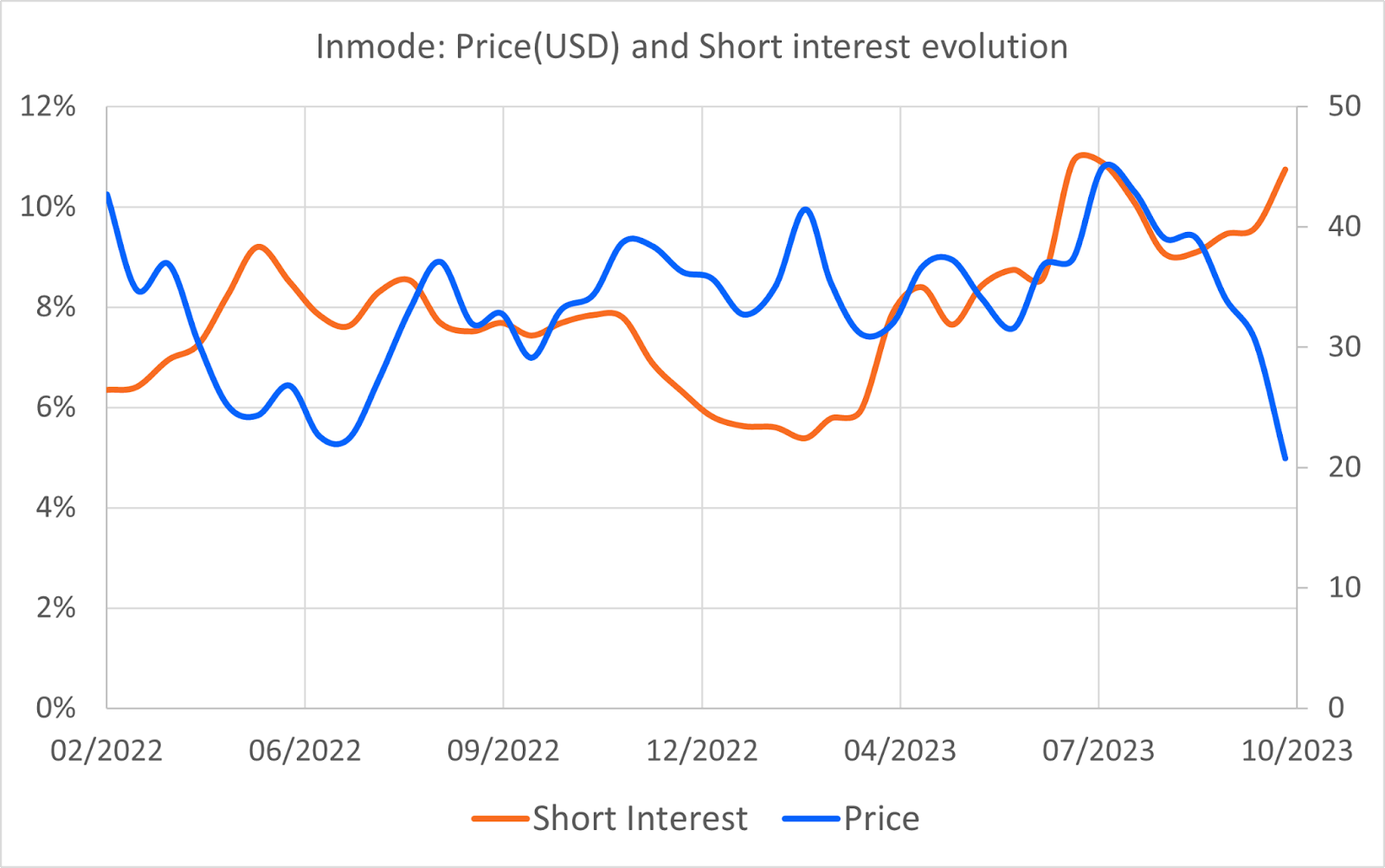

Short interest

Short interest has increased since Inmode’s price drop.

It has gone back up to levels seen in July of this year of about 11% of the shares outstanding. Data is only provided twice a month.

Since the 13th of October when I published my deep dive, one analyst has changed his rating from a buy to hold (not because of my deep dive I assure you! 🙂). Just to show if analyst have changed their stance.

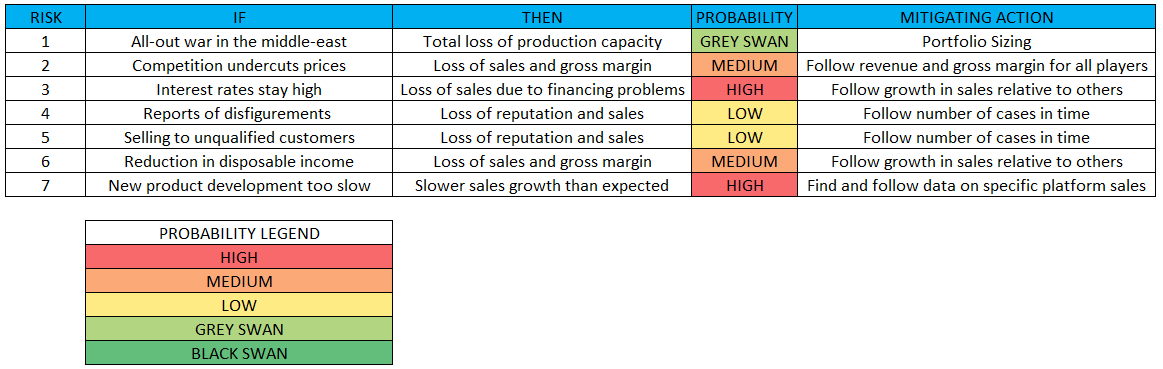

Short thesis - risk analysis

As promised, because I’m long, it is important to try to take the other point of view and analyze the short thesis and associated risks. My goal here is to list all the risks and try to answer them based on data points or reasoning. For each risk, the structure will be:

Explain the risk -> IF this happens THEN state the consequence

My take on the risk, the likelihood of occurrence

What can we do? List possible mitigation actions

Let’s go:

The Israël conflict

Risk: IF the conflict in Israël erupts into a full-scale war THEN business could be severely impacted.

My take: I truly hope that some form of peace can be found. Israël and the United States do not want this to become a full-scale war. Although the US stands by Isräel, they have tried to negotiate and mitigate the ground assault. De-escalation is not immediately on the horizon but I’m optimistic they’ll get there. An all-out war would be a sort of black (or grey?) swan event. It is not impossible but unlikely.

What can we do? The only real way to protect against this is in portfolio sizing. Size accordingly.

Competition

Risk: IF Competition from other companies increases and starts to undercut Inmode’s prices THEN Inmode might lose sales in the future.

My take: This is one of the most important risks with a high probability, but one should not underestimate the sales network that Inmode has built over the past decade. Physicians pay immediately or finance typically through a 5-year lease. Customers from 2018 or earlier seeing their lease expiring may want to update their platforms. If they are satisfied and are already a customer, Inmode might have a slight advantage. The situation is different for future new customers.

What can we do? Track sales volume and gross margin for Inmode AND its competitors. If Inmode has to reduce its prices, then the gross margin will be impacted.

Interest rates

Risk: IF Interest rates stay high or continue rising THEN financing possibilities for physicians will decrease with a decrease in sales

My take: This risk is already a reality but, it is the same for the entire sector and not specifically focused on Inmode. Management has stated that in certain regions, they are actively working with banks to come up with financing solutions that they can directly offer to their customers. This is a great proactive approach. But this is indeed a risk that could lead to a slowdown in sales. The question then is, if the impact is on the entire sector, will Inmode’s sales slow down faster or slower than their competitors?

What can we do? Measure the growth of sales for Inmode versus its closest competitors to verify their growth rate on a relative scale.

Horror stories

Risk: IF certain treatments lead to disfigurement or something similar THEN Inmode’s reputation could be tarnished with a loss of sales as a consequence.

My take: After publishing my deep dive, I was sent pictures of procedures performed with microneedling and the Morpheus8 that ended badly. First off, the information that was sent was 3 years old. As I stated in my deep dive, I did find isolated reports of this on the internet, but they remain isolated. Inmode has an installed basis of about 17,000 platforms. Regulatory approval and clinical studies are needed to provide proof of work. If there was something materially wrong with their products, then sales would not have increased over the last years as they have.

What can we do? Other than keeping our eyes open for an increase in the volume of these kinds of stories, I do not see another way to mitigate this risk.

Overreaching

Risk: IF Inmode starts aggressively selling to non-qualified customers THEN this could lead to inappropriate use of Inmode’s products with possible bad outcomes and loss of reputation and sales as a result.

My take: There are reports of Inmode selling to dentists who have had no formal training in aesthetic treatments of the skin. I cannot verify if these reports are true or not, but if future headwinds lead to Inmode actively disregarding the qualifications of the customer, or selling to anyone, I would consider it a red flag and consider this a violation of business conduct integrity.

What can we do? Be on the lookout for additional reports.

Economic Slowdown

Risk: If future economic headwinds come true and people’s disposable income reduces THEN this could lead to a drop in demand for aesthetic treatments

My take: A micro-needling treatment can vary from 1500 to 5000 USD depending on the country and the number of treatments that are needed. People who decide to undergo these treatments are pretty affluent. New physicians might postpone a possible purchase because demand decreases. Up until Q2 2023, Management has stated they saw no such decline in demand. I believe there might be some slowdown, but this could be mitigated by the fact that the end customer is affluent enough so that he or she can continue their treatment. A second argument is that because Inmode is selling new platforms in Women’s Wellness and Ocular treatment, these can be less sensitive to an economic downturn because they may be able to solve real medical problems.

What can we do? Inmode does not release sales by platform, so we cannot investigate how well the new platforms are doing. We can only look at how sales numbers in total will evolve in the future and compare them to competitors.

One-trick pony

Risk: IF Inmode cannot grow its new product sales fast enough, THEN sales growth will slow down in the medium term.

My take: Inmode has several products, and although they do not specify sales numbers by platform, the Morpheus8 is by far their flagship product. The roll-out of their new product line into Women’s Wellness and Ocular Care is going more slowly than expected. This is a concern with a high degree of probability. The other side of it is a certain degree of optionality if Inmode succeeds in developing and marketing a 2nd flagship product.

What can we do? Try to find some information about platform-specific sales. Follow sales numbers.

If you see other risks that I have not covered, please let me know by mail or in the comments!

Here are all the risks with their probabilities:

With the previous risks mentioned in the deep dive (for example impact of GLP-1 drugs) and this latest risk analysis, we can construct our selling rules or our method to track the future performance of the company.

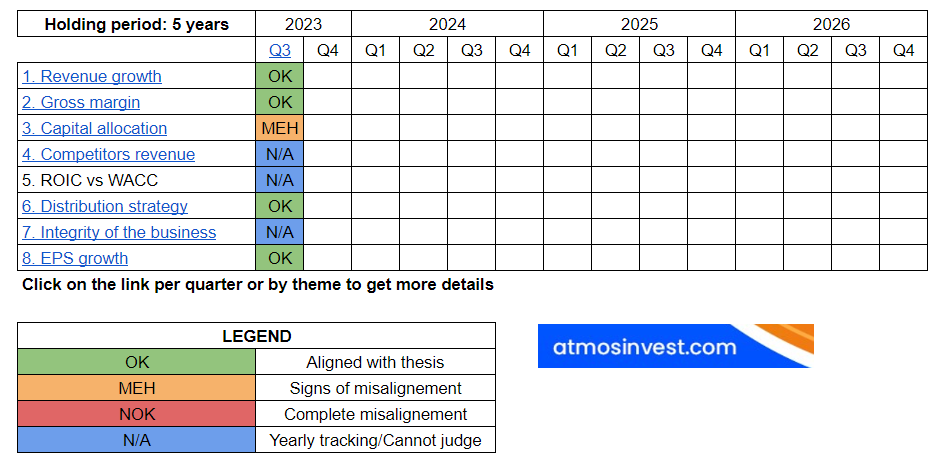

Selling Rules, tracking Inmode

Based on the risk analysis and Inmode deep dive, these are the indicators we are going to track:

Revenue: Sales is the lifeblood of the company. My thesis expects a better-than-no-growth scenario. This means that a slowdown in growth is acceptable, but a slowdown until 0 growth year over year is not OK. The goal is to track this from quarter to quarter but one decline in one quarter is not enough to break the thesis. A significant slowdown needs to be observed over a longer period before reassessing the investment. It will be important to understand why this slowdown occurs and how candid management will be about the reasons.

Gross margin: Inmode has very high gross margins. If margins start to decrease, this can be a sign that they are reducing their sales prices to compete. This is of course a very bad sign. If possible, except for a scale economies shares business model, one should avoid competition on price.

Capital allocation: At the minimum, we would like to see buybacks that offset the employee incentive plan. In the best case, a significant buyback program to reduce the share count. But based on the past, and looking at the current conflict in Israël and the rise of interest rates, my hunch is that management in the short term will remain conservative and keep the cash pile at hand. They have built a war chest of cash to weather a storm. They may be prudent and wait to see if the weather is turning before starting to deploy this cash in a buyback.

Revenue of other competitors: Compare the evolution of revenue to its competitors to see any effect on the overall slowdown and to verify if growth for Inmode is slowing down faster or slower than the others.

ROIC versus WACC: Besides sales growth, we need to check if Inmode continues to make a return on invested capital beyond the WACC. This will be done once a year.

Distribution strategy: As I have previously written, the main competitive advantage Inmode has is its wide distribution network to 92 countries with in several cases a direct sales team. We want to see this grow and see an increase in direct sales if possible.

Integrity of the business: Track to see if there is an increase in reporting on bad outcomes of procedures or selling to dentists. Although it might be difficult to ascertain the truth behind these reports, if there is a spike or increase in the number of these reportings, this could be a bad signal that maybe Inmode is overreaching its sales strategy.

EPS growth rate: Because this remains one of the most important drivers of value and performance.

Notice that there is no selling rule for price. My goal is to focus mainly on sales and underlying fundamentals related to the business and the industry.

Are there rules missing? Would you add or remove something? Let me know.

The result looks like this for the 3rd quarter of 2023:

You can access the Google Sheets page here. You’ll find more detailed information on Inmode and how I assessed Inmode’s performance.

Conclusion

I learned a lot by doing this risk analysis. It has helped me improve the way I will track the company in the future. Although I always feel like defending my position because I’ve taken a long thesis, I try to be conscious of possible biases and actively look at the opposite view.

If you like this article and the way it resulted in a company tracker, please consider sharing.

You can find all previous information on Inmode here

The previous deep dive is also available in PDF form but hasn’t been updated yet with all the additional information. I will let you know when it is ready.

Don't you think the comments around share buybacks are pretty damning? The reasoning makes no sense. Either they are 1) stupid, 2) lying, and/or going to blow the cash on bad m&a.